Step.1 Estimate the equation as usual.(ls y c x)

Step.2 Name the residual as E (genr e=resid)

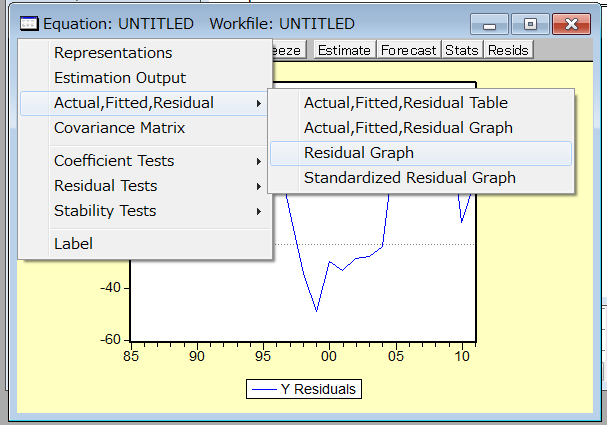

Step.3 View the residual Graph to detect auto-correlation

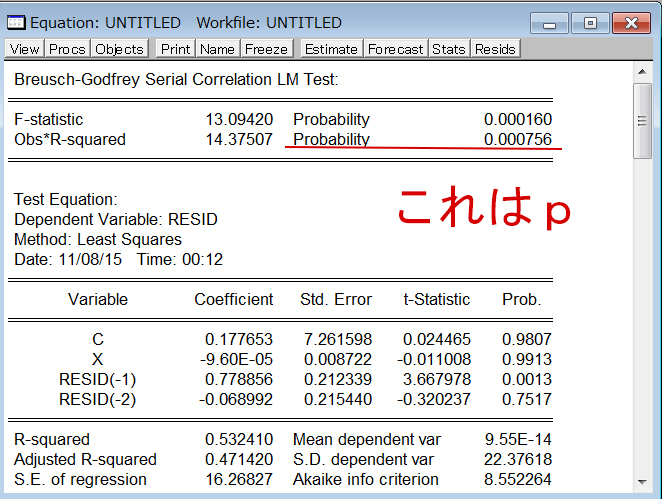

Step.4 Do Serial Correlation LM Test to check the possibility of auto-correlation.

Step.5 Estimate GLS equations by using the Cohrane-Orcutt method.

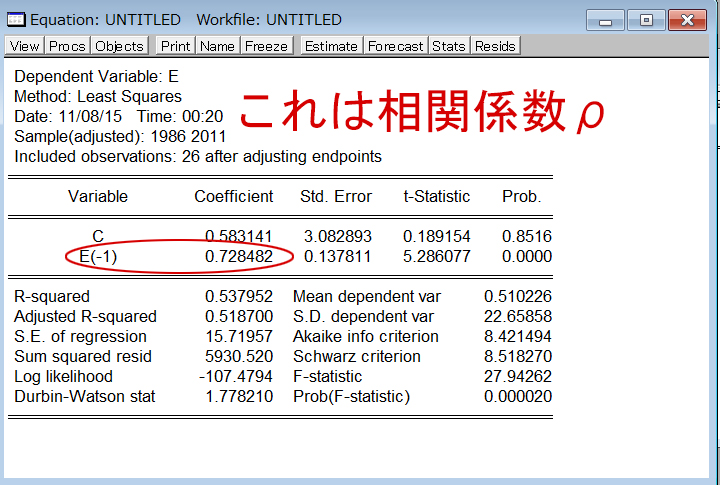

1) In order to get the ρ, estimate the equation of e e(-1) ( ls e e(-1))

2) ls y-(ρ’s value)*y(-1) c x-(ρ’s value)x(-1)

3) c^=c/(1-ρ)

Step.6 Get the equation